Cisco System's Earnings Preview: Will the Tech Titan Surpass Expectations Amidst AI and Splunk Integration?

Alex Vellor

Alex Vellor

Tech giant Cisco Systems (NASDAQ: CSCO) is gearing up for an important event today, February 12th, when it reveals its second-quarter earnings results after the market closes.

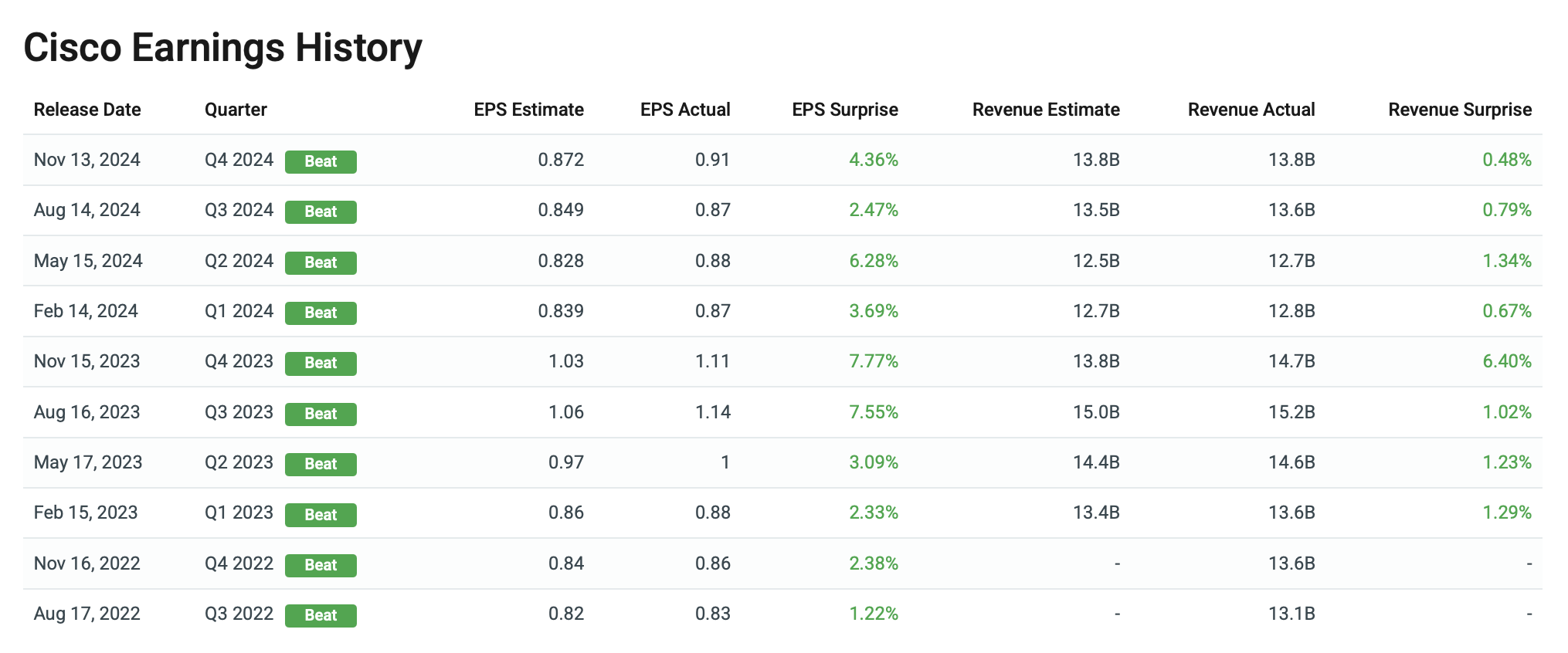

Analysts predict a promising 8.4% revenue increase, expecting the figure to hit $13.87 billion, alongside earnings per share coming in at $0.91. The anticipated growth is attributed to a surge in demand for data center solutions, an uptick in orders, and the fruitful integration of Splunk—a development that could serve as significant momentum for the company.

However, not all forecasts align. Analysts at Barclays project a slightly conservative outlook with an estimate of 8% revenue growth for the quarter. The focus here is anticipated to be primarily on order growth, the significance of Splunk, and the impact of AI-related developments.

Conversely, the projections from Morgan Stanley spell a more optimistic tale, hinting at a possible revenue surprise spurred by unexpectedly strong networking performance. They anticipate a notable year-over-year uptick in orders, likely in the mid-to-high teens range for inorganic growth and low single digits for organic growth. Splunk’s performance is also expected to exceed initial expectations this quarter.

Citi's analysts are joining the enthusiastic chorus, having recently initiated a 30-Day Catalyst Watch on Cisco. Following two-quarters of positive sequential growth, analysts believe that Cisco's previous lackluster sales (-13% year-over-year in Q4 2023) is setting the stage for potential upturns in the January quarter, possibly even leading to a revised forecast for fiscal 2025.

While maintaining a Market Perform rating, analysts at Raymond James are aligned with cautious optimism that anticipates Cisco will meet its quarterly forecasts, spurred by improvements in federal orders and overall order growth. They noted that Splunk's operational synergies and imminent restructuring present a likely avenue for increased profitability, although the company’s position in the AI market remains a hotly debated topic. Nonetheless, they see Cisco as a company well-poised for long-term success amidst an encouraging IT spending outlook.

Interestingly, historical performance shows Cisco's strong propensity to outshine estimates—an impressive track record of hitting both top and bottom lines for two consecutive years.

In the last three months, analysts have provided a flurry of upward revisions—19 for EPS and 14 for revenue estimates.

Last quarter, Cisco surprised the market with better-than-expected results and has projected sales between $13.75 billion and $13.95 billion for the upcoming period. Adjusted earnings are anticipated in the range of $0.89 to $0.91 per share.

When contemplating the implications for investors, the $24 billion acquisition of Splunk serves as a pivotal point. It has since shifted Cisco’s security division to account for 15% of total revenue, reversing a stagnant growth trend that had plagued this sector for years. Meanwhile, the legacy networking division, although it constitutes half of Cisco’s revenue, has faced its own turmoil, with figures declining from $9.5 billion in July 2023 to $6.75 billion by October 2024.

Cisco is not completely on the sidelines of the AI boom. In fiscal Q1 2025, the company secured $300 million in AI orders and is on course to reach the $1 billion mark by fiscal year-end.

Investors looking to stake a claim in Cisco must be prepared for a test of patience. Since the dawn of the millennium, the stock has delivered a meager annual return of just over 2%, although it has seen a relative improvement of 9.5% since 2010—both figures lagging behind the S&P 500.

One notable trend that’s caught the eye of many is Cisco’s non-correlation with the dominating tech giants and semiconductor leaders. Intuitively, this might suggest it could weather bear markets better than most, avoiding the pitfalls of being too closely tied to momentum trades. Yet, the reality was starkly different in 2022, when Cisco itself plummeted 28% from January to July, suffering a steeper decline than the overall market.

About The Author

Alex Vellor

Read Next in Latest Stock Market News

View All News