Lululemon (LULU) Heads Into Q4 Earnings With Big Questions Hanging

Alex Vellor

Alex Vellor

Shares of Lululemon Athletica (LULU) are navigating choppy waters ahead of their Q4 fiscal 2025 earnings report scheduled for today, March 17.

This year hasn't been kind to the brand, with the stock dropping around 24% since January and sliding more than 50% over the past year. The stage is set for a revealing quarter that could confirm whether the retailer's recent troubles are temporary blips or deeper issues.

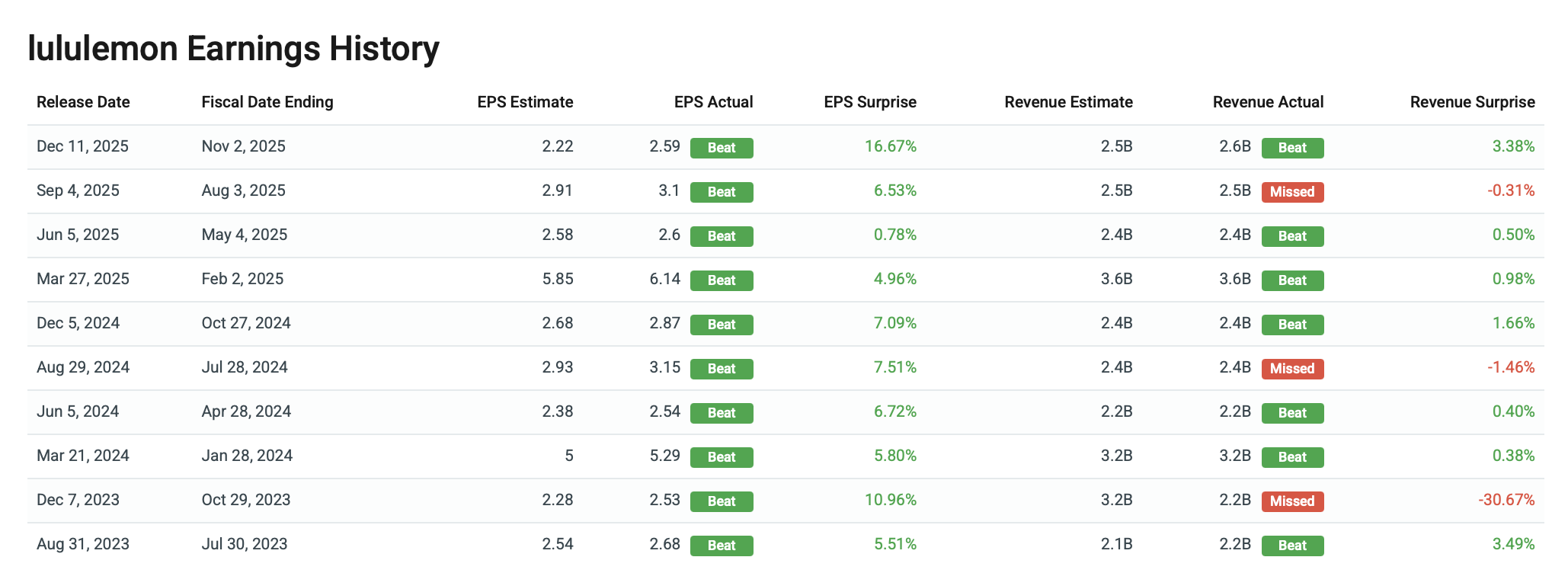

The market expects a 22% plunge in earnings per share to $4.78, accompanied by slightly declining revenue, forecasted to drop about 1.1% to $3.57 billion. Despite these numbers, Lululemon hinted earlier this year that it might beat guidance thanks to robust holiday season sales, energized by Black Friday deals and new product launches. Heavy store traffic was noted as a positive signal, but whether this momentum will carry through remains uncertain.

One wild card that could move the needle is the pending CEO transition. Calvin McDonald, who has steered the ship since 2018, plans to step down, with his advisory role concluding at the end of March. Investors will be watching closely for any announcements about his successor made alongside the earnings release, as fresh leadership might shake up sentiment.

International growth remains a bright spot amid domestic headwinds. Lululemon has been methodically increasing store openings beyond North America, with a focus on markets like China and Mexico. While U.S. growth slows and has forced a cut in guidance, these overseas expansions may offer a lifeline, fueling future sales gains.

The stock's valuation also stands out in this tussle. With a forward price-to-earnings ratio hovering near 12, Lululemon trades at a discount compared to sector peers, averaging closer to 16. This compressed valuation hints that the recent negativity could already be reflected in the stock price, leaving room for a re-rating if the company delivers on or above expectations.

Yet, risk factors loom large. The threat of recession, ongoing inflationary pressures, and tightening budgets among less affluent shoppers could temper enthusiasm for premium athleisure. Plus, competition is heating up as more brands chase the lucrative activewear segment, pressuring profit margins and sales growth alike.

Wall Street's consensus remains cautious, with analysts mostly holding onto their shares and pricing in a roughly 30% upside against today's levels. However, with sentiment swinging so widely this year, even small surprises in earnings or guidance could provoke outsized moves one way or the other.

So when the results drop, will Lululemon's international bets and leadership shuffle be enough to turn the tide? Or is this athlete just running out of steam? The next few days should offer a clearer picture.

About The Author

Alex Vellor

Read Next in Latest Stock Market News

View All News