Verizon Q2 Preview: Will a £130B UK 5G Deal Impact Its Performance?

Alex Vellor

Alex Vellor

Verizon Communications Inc. (VZ) is gearing up to release its Q2 2025 earnings on July 21, with the analysts' Consensus Estimate pegged at $33.6 billion in revenue and $1.18 a share in earnings. Over the past month, earnings forecasts for 2025 have nudged down slightly from $4.69 to $4.68 per share, while 2026 numbers have inched up from $4.86 to $4.90.

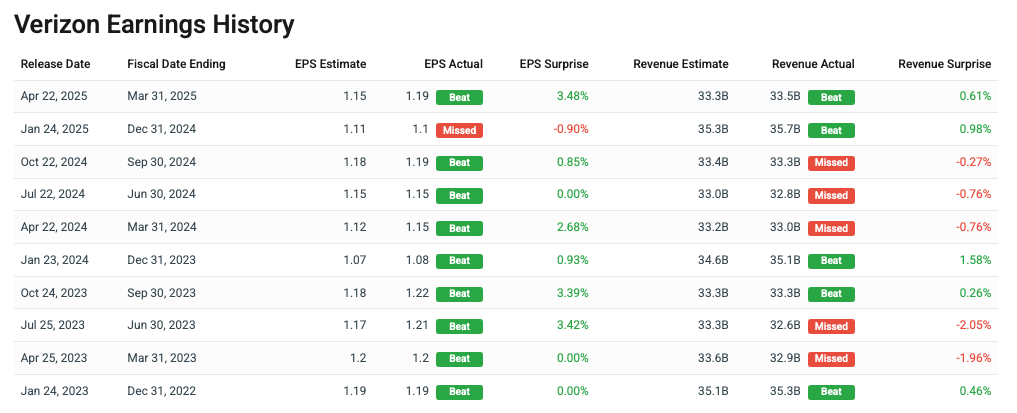

Verizon has historically outpaced expectations, boasting a solid run of earnings surprises over the last four quarters, averaging a 1.53% beat. The last quarter was no exception, with a 3.48% upside.

The company's mix-and-match pricing strategy on wireless and home broadband plans continues to push adoption of 5G devices and premium unlimited plans. It has also shaken up streaming bundles, letting customers pick and choose content they're actually interested in-careful eye to keeping bills lean.

One highlight this quarter: snagging a multibillion-dollar deal to build a Private 5G Network along the River Thames Estuary in the UK, an area that handles about £130 billion of maritime trade annually. This private network aims to connect key logistics, manufacturing, and innovation hubs with scalable infrastructure supporting advanced data, AI, edge computing, and IoT-which could redefine port operations and industrial processes.

On the domestic front, Verizon rolled out its network slicing technology for first responders across 20+ markets, now available anywhere Verizon offers 5G Ultra Wideband. The Frontline Network Slice offers dedicated 5G bandwidth to public safety teams, promising better reliability and scalability in real time. This likely bumped customer sign-ups and churn reductions in the Consumer segment, which is forecasted at around $25.69 billion for this quarter-right in line with modeled expectations of $25.63 billion.

In the Business segment, Verizon launched its Edge Transportation Exchange, a state-of-the-art vehicle-to-everything (V2X) mobile network platform. Using its 5G and LTE infrastructure combined with edge computing tech, this platform enables connected vehicles to communicate critical data faster and more reliably. Business segment revenue estimates sit near $7.26 billion, with models projecting a similar $7.29 billion.

That said, not everything looks positive. Headwinds from unfavorable foreign currency movements, hefty investments in 5G infrastructure, and elevated operating costs are likely weighing on profit margins. Verizon's three-year price lock on core calling, data, and texting plans (excluding taxes and fees) signals a customer-friendly approach but also could pressure future margins given the discounts and promotions in play. On the legacy front, the wireline division continues to bleed, as VoIP alternatives and aggressive triple-play offers from cable companies erode traditional access line revenues.

Verizon’s upcoming earnings on July 21 will be critical. Recent commentary highlights ongoing improvements, including debt reduction, integration of the Frontier acquisition, and growth catalysts such as AI Connect initiatives, which could support future EPS growth and solidify Verizon’s defensive income thesis. However, the recent slight price drag may reflect market caution ahead of earnings, given general sector pressures and broader tech sell-offs.

VZ Stock Earnings Preview:

| Release date | Jul 21, 2025 |

| EPS estimate | $1.18 |

| Revenue estimate | 33.472B |

| Expected change | +/- 3.55% |

About The Author

Alex Vellor

Read Next in Latest Stock Market News

View All News