Discounted Cash Flow (DCF) Analysis: A Comprehensive Guide for Evaluating Investments

Discounted Cash Flow (DCF) analysis is like the ultimate secret weapon in finance—a game-changer for anyone looking to make serious money. Picture this: you’re estimating the future cash flows of an investment and then discounting them back to the present, giving you the real, unvarnished value of an asset. This isn't just about numbers; it's about seeing through the noise and spotting opportunities others might miss. The real kicker? The Net Present Value (NPV). This is where the rubber meets the road, showing you whether an investment is a gold mine or a money pit. With DCF, you're not just guessing—you're making informed, strategic decisions that separate the winners from the wannabes.

Core Concepts: Time Value of Money and DCF Formula

The time value of money principle suggests that a pound today is worth more than a pound in the future due to its potential earning capacity. DCF analysis discounts future cash flows to their present value, allowing for a precise evaluation of an investment's worth.

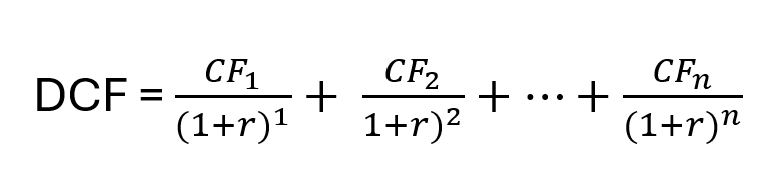

DCF Formula

Where:

CF = Cash flow

r = Discount rate (e.g WACC / Weighted Average Cost of Capital)

n = year (e.g first Cash Flow year = 1)

Conducting a DCF Analysis: Step-by-Step

1. Forecasting Future Cash Flows

Future cash flows (FCFs) are forecasted by calculating the Free Cash Flow, which is the cash flow available to investors after accounting for capital expenditures (Capex), working capital changes, and taxes.

For example, consider a company investing in new machinery, to facilitate understanding, here are the data assumptions to consider:

- EBIT: $300,000

- Tax Rate: 26.5%

- Depreciation: $100,000

- Capex: $1,000,000 (initial investment)

- Change in Working Capital: $0 (assumed for simplicity)

FCF = EBIT(1−Tax Rate) + Depreciation – Capex − Change in Working Capital

FCF=300,000 × (1−0.265) + 100,000 − 1,000,000 − 0

FCF=(300,000×0.735) + 100,000 − 1,000,000

FCF=220,500 + 100,000−1,000,000

FCF=320,500−1,000,000

FCF = −679,500

In this scenario, the company initially faces a hefty negative free cash flow of $679,500, thanks to the big spend on new machinery. But don't let that scare you—this is a classic case of spending money to make money. The positive EBIT and depreciation tell us that, over time, as the company rakes in more revenue, that big investment in machinery is going to start paying off, flipping the cash flow to positive. This is a prime example of why timing and scale of cash flows are crucial when you're sizing up an investment. It's not just about the numbers now—it's about the potential down the road.

2. Determining the Discount Rate

The discount rate, often represented by the Weighted Average Cost of Capital (WACC), reflects the opportunity cost of capital and the risk associated with the investment. For a company with 60% equity and 40% debt, a cost of equity of 10%, and a post-tax cost of debt of 5%, the WACC would be:

Cost of equity (Capital Asset Pricing Model - - CAPM):

Cost of Equity=Risk Free Rate + β×(Market Return−Risk-Free Rate)

Assume the following values:

- Risk-Free Rate: 2% (The return on risk-free investments, like government bonds).

- Beta (β): 1.6 (A measure of the stock's volatility relative to the market. A beta of 1 means the stock moves with the market, greater than 1 means more volatile, and less than 1 means less volatile).

- Market Risk Premium: 5% (The average return expected from the market e.g S&P500 Expected return).

Cost of Equity (CAPM) = 2% + (1.6 × 5%)

Cost of Equity=2% + 8%

Cost of Equity=10%

Now let's calculate the WACC :

WACC = (0.6×0.10) + (0.4×0.05) = 0.08 or 8%

This means that the company needs to generate a return of at least 8% on its investments to satisfy its investors and lenders. This percentage represents the minimum average return expected by those providing capital, such as equity investors and debt holders.

3. Calculating Present Value of Cash Flows

Each cash flow is discounted back to its present value using the formula, accounting for the time period and the discount rate. This calculation provides the present value of each cash flow, which when summed, gives the total DCF value.

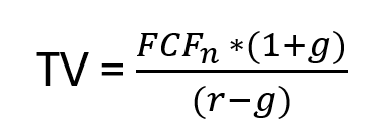

4. Calculating the Terminal Value

Terminal value (TV) captures the value beyond the forecast period. It is crucial as it often constitutes a significant portion of the DCF value. The terminal value can be calculated using the Gordon Growth Model:

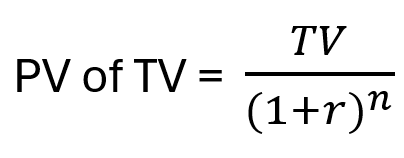

Where g is the perpetual growth rate, typically aligned with long-term economic growth expectations. This value is then discounted back to the present value using the formula:

Example Calculation: Summing Cash Flows and Terminal Value

Consider a company A, with the following data:

- Forecasted Free Cash Flows:

Initial Capex: $500 million

Year 1 FCF: $40 million, growing at 5% annually

Depreciation: $10 million annually

- Discount Rate:

WACC: 8% (Calculated previously)

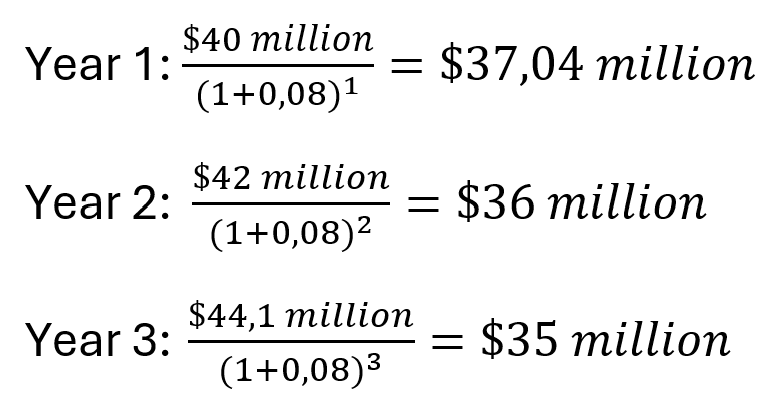

- Year-by-Year Cash Flow Calculation:

Year 1: FCF1 = $40 million

Year 2: FCF2 = $42 million (5% growth)

Year 3: FCF3 = $44.1 million (5% growth)

Present Value of Cash Flows (PVCF):

Sum of PVCF: $37,04 + $36 + $35= $108,04 million

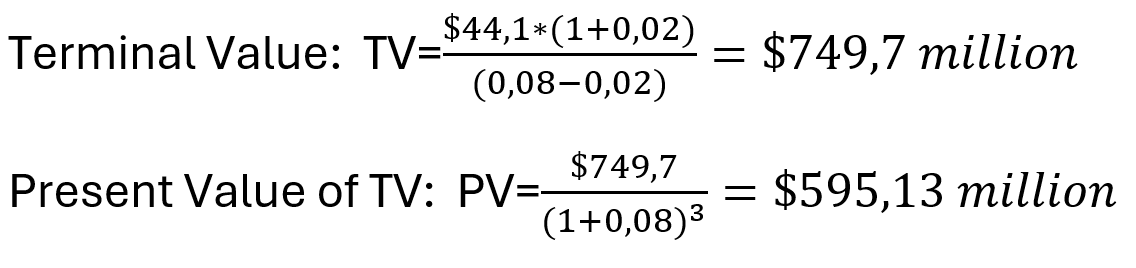

- Terminal Value Calculation:

- Terminal FCF: Assume the year 3 FCF ($44.1 million) continues to grow at 2% perpetually.

- Total Present Value:

Adding the PVCF and PV of TV: $108,04 + $595,13 = $703,18 million

Conclusion: NPV and Investment Decision

The total present value of $703.18 million, set against the initial investment of $500 million, yields a net present value (NPV) of $203.18 million. This positive NPV isn't just a number—it's a green light, a signal that this investment is not just viable but lucrative. It tells us that, after covering all costs, we're looking at a surplus of $203.18 million in today's terms.

Limitations of the DCF Model

1. Dependence on Forecasts and Assumptions

DCF relies heavily on the accuracy of future cash flow projections, discount rates, and growth assumptions, which can be difficult to estimate accurately.

2. Estimating Terminal Value

Terminal value calculations can significantly impact the DCF valuation, especially if the growth rate or discount rate assumptions are off.

3. Complexity and Accessibility

DCF analysis requires a deep understanding of finance, making it complex and potentially inaccessible for non-experts. Furthermore, it does not account for market conditions, such as investor sentiment or economic cycles.

Key Takeaways

- Valuation with DCF: Discounted Cash Flow (DCF) analysis helps determine the value of an investment by estimating its future cash flows.

- Present Value Calculation: The present value of expected future cash flows is determined using a projected discount rate.

- Investment Viability: If the DCF is higher than the current cost of the investment, the opportunity could result in positive returns, indicating it may be worthwhile.

- Use of WACC: Companies often use the Weighted Average Cost of Capital (WACC) as the discount rate because it reflects the rate of return expected by shareholders and accounts for the cost of both equity and debt.

- Reliance on Estimates: A limitation of the DCF method is its dependence on estimates of future cash flows, which can be uncertain and potentially inaccurate.

About The Author