Tesla's Q1 Earnings Preview: Robotaxi Expansion and Surging Capex Take Center Stage

Alex Vellor

Alex Vellor

Tesla's shares have faced headwinds this year, and all eyes are on the upcoming Q1 earnings report Wednesday after the market closes. The spotlight is on Tesla's progress with its Robotaxi service and a dramatic spike in capital expenditure that's raising eyebrows across Wall Street.

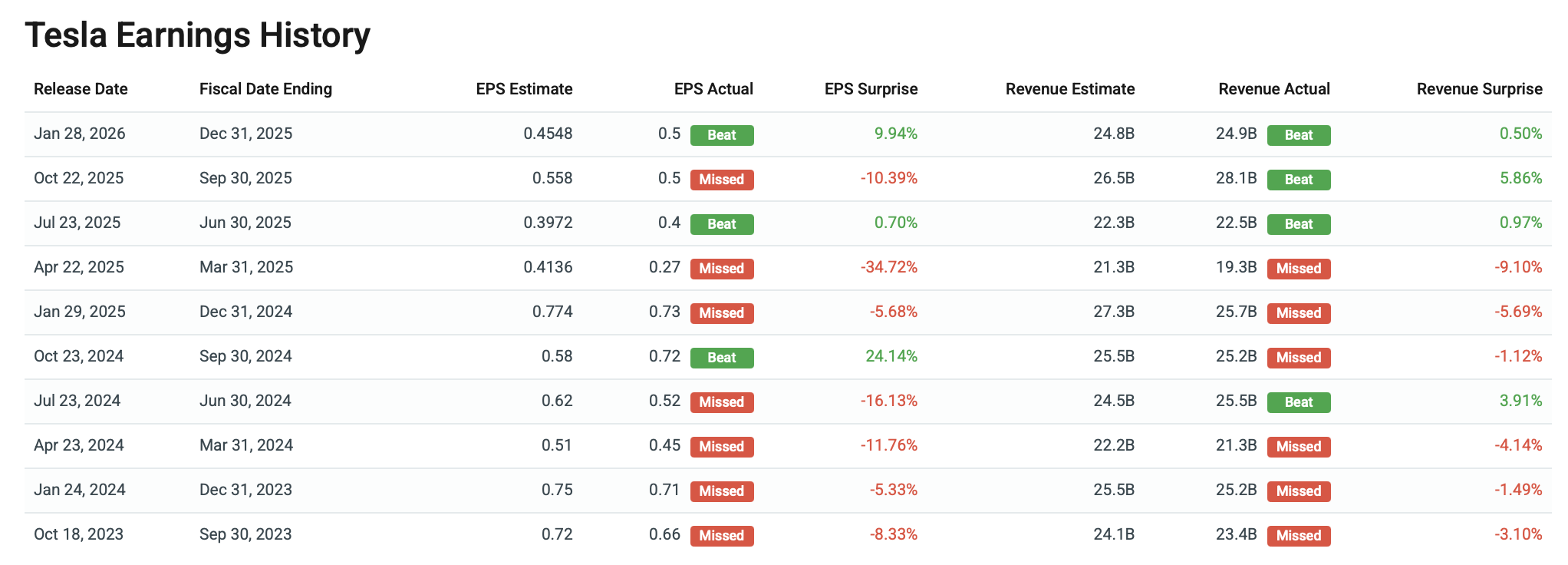

Consensus estimates foresee Tesla posting revenues around $22.08 billion, marking a 9% decline compared to the same quarter last year. Adjusted earnings per share are expected near $0.35, while EBITDA is forecasted to drop 14.4% to about $3.217 billion. These numbers suggest Tesla's growth engine might be sputtering slightly, but the company's push into autonomous ride-hailing could be the spark investors hope for.

This weekend, Tesla expanded its Robotaxi operations beyond Austin to include Dallas and Houston. Notably, the company emphasized that the rides in these new cities operate in "unsupervised" mode, meaning no safety driver is present, which is a step up from the limited supervised trips previously conducted in Austin. However, the company remains tight-lipped about the actual fleet size and number of unsupervised vehicles, leaving analysts to read between the lines on user adoption and safety metrics.

BofA Securities' Alexander Perry reiterated his buy rating with a $460 price target, emphasizing Tesla's Robotaxi as a major disruptor in the $1 trillion+ rideshare market. Perry views Tesla's approach as an early monetization phase of its autonomous driving work. Rival players like Uber and Waymo add a layer of competition, but Tesla's entry with unsupervised rides signals a clear intent to challenge the status quo.

Morgan Stanley highlighted Tesla's looming milestone of accumulating over 10 billion full self-driving miles. This massive data trove could be the key to accelerating breakthroughs in autonomy and scaling the Robotaxi service. Despite a slow start, the company's strategic focus on new city launches points to a patient, long-term vision.

On another front, Tesla's capital expenditures are set to surge, with guidance pointing to over $20 billion this year - more than double last year's $8.5 billion spend. The cash burn is expected to push free cash flow into negative territory. This hike is largely tied to investments in batteries, Cybercab production, the Optimus robot project, and crucially, chip manufacturing. Elon Musk recently revealed Tesla is "taping out" its AI5 chip design, a foundational move for future vehicles, massive AI training clusters, and the Optimus robots.

The new AI5 chip will be produced at Tesla's planned Terafab facility. While ambitious, analysts caution the venture to build an in-house fab presents enormous technical and financial hurdles. Production isn't scheduled to start until 2029, with scaling afterward. Bernstein analysts have thrown out staggering capital estimates ranging between $5 trillion and $13 trillion, underscoring the enormous scale of this project.

Besides these tech and manufacturing strides, Tesla's core auto business is still in the mix. The company hinted at launching a more affordable model to refresh its current lineup, which could influence unit sales. Q1 deliveries clocked in at 358,023 vehicles, slightly below estimates but still up 6.3% year-over-year. Last year's baseline was low due to the Model Y transition, so the comparables are a bit skewed.

All in all, Tesla's Q1 report will ignite plenty of discussion - from how soon Robotaxis can grab meaningful market share to whether the colossal capex outlay will translate into future gains, or just weigh down margins for now.

About The Author

Alex Vellor

Read Next in Latest Stock Market News